Protecting Your Legal Career: Insurance Shields Lawyers, The legal profession is inherently fraught with risks. Lawyers navigate complex cases, manage client expectations, and operate in a litigious environment where mistakes or perceived missteps can lead to lawsuits. Malpractice claims, ethical disputes, or even frivolous lawsuits can jeopardize a lawyer’s reputation, financial stability, and career. To mitigate these risks, professional liability insurance—commonly known as malpractice insurance—serves as a critical shield for legal practitioners. This article explores how insurance protects lawyers from lawsuits, the types of coverage available, the risks they face, and the broader implications for the legal industry.

The High-Stakes World of Legal Practice

Lawyers face unique vulnerabilities due to the nature of their work. A single oversight, such as missing a filing deadline, misinterpreting a statute, or failing to anticipate a client’s needs, can trigger a malpractice claim. According to the American Bar Association (ABA), approximately 4-6% of practicing attorneys in the United States face malpractice claims annually, with higher rates in high-risk practice areas like personal injury, real estate, and family law. Beyond malpractice, lawyers may also encounter lawsuits alleging breach of fiduciary duty, conflicts of interest, or fraudulent misrepresentation.

The financial and emotional toll of defending against a lawsuit can be immense. Legal defense costs, including attorney fees and court expenses, can escalate quickly, even if the claim is baseless. Moreover, a lawsuit can damage a lawyer’s reputation, leading to lost clients and diminished professional standing. For solo practitioners or small firms, the consequences can be particularly devastating, potentially leading to bankruptcy or closure.

The Role of Professional Liability Insurance

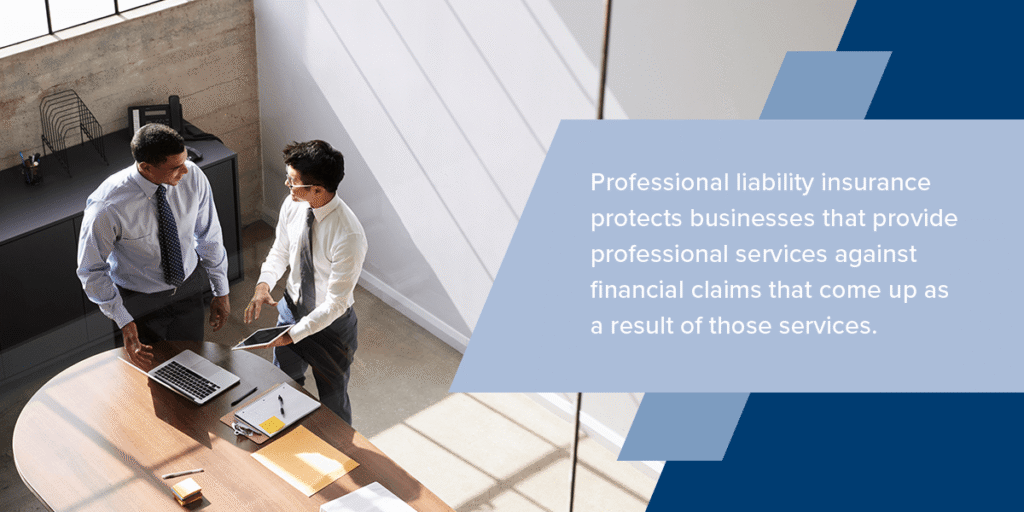

Professional liability insurance is designed to protect lawyers from the financial and professional fallout of lawsuits. This type of insurance typically covers claims arising from errors, omissions, or negligence in the provision of legal services. It serves as a safety net, ensuring that lawyers can continue practicing without the constant fear of financial ruin from a single claim.

Key Components of Malpractice Insurance

- Defense Costs: One of the most significant benefits of malpractice insurance is coverage for legal defense costs. These include attorney fees, court costs, expert witness fees, and other expenses incurred while defending against a claim. Even if a lawsuit is dismissed, defense costs can run into tens of thousands of dollars, making this coverage indispensable.

- Damages and Settlements: If a claim is successful or settled out of court, insurance can cover the cost of damages awarded to the plaintiff, up to the policy’s limits. This protects lawyers from having to pay out of pocket for judgments or settlements.

- Regulatory and Disciplinary Proceedings: Some policies extend coverage to costs associated with defending against disciplinary actions by state bar associations or other regulatory bodies. These proceedings can arise from ethical complaints and may carry significant professional consequences.

- Reputational Protection: By resolving claims efficiently, insurance can help mitigate reputational damage. Insurers often provide access to experienced defense counsel who specialize in legal malpractice cases, increasing the likelihood of a favorable outcome.

Types of Malpractice Insurance Policies

Malpractice insurance policies vary in scope and structure, allowing lawyers to choose coverage that aligns with their practice’s needs. Common policy types include:

- Claims-Made Policies: These policies cover claims made during the policy period, regardless of when the alleged incident occurred, provided the lawyer had coverage at the time of the incident. Most legal malpractice insurance is written on a claims-made basis.

- Occurrence-Based Policies: Less common in legal malpractice insurance, these policies cover incidents that occur during the policy period, regardless of when the claim is filed. These are more prevalent in other professions, such as medicine.

- Tail Coverage: Also known as extended reporting period coverage, tail coverage protects lawyers after a claims-made policy expires, provided the claim arises from an incident that occurred during the policy period. This is critical for lawyers who retire, change firms, or switch insurers.

- Prior Acts Coverage: This covers claims arising from work performed before the current policy’s inception, as long as the lawyer was insured at the time and no known claims existed.

Common Risks Covered by Insurance

Malpractice insurance addresses a wide range of risks that lawyers encounter. Some of the most common scenarios include

- Errors and Omissions: Mistakes such as incorrect legal advice, drafting errors, or missed deadlines are among the leading causes of malpractice claims. For example, a lawyer who fails to file a lawsuit within the statute of limitations may face a claim for professional negligence.

- Breach of Fiduciary Duty: Lawyers have a fiduciary duty to act in their clients’ best interests. Allegations of self-dealing, conflicts of interest, or failure to disclose pertinent information can lead to lawsuits.

- Client Miscommunication: Misunderstandings about case outcomes, fees, or legal strategies can result in claims. Clear communication and documentation are essential, but insurance provides a fallback if disputes escalate.

- Frivolous Lawsuits: Even baseless claims require a defense, which can be costly. Insurance ensures that lawyers can address these lawsuits without draining personal or firm resources.

- Cybersecurity Breaches: With the rise of digital legal practice, cyberattacks targeting client data are a growing concern. Some malpractice policies include cyber liability coverage to address losses from data breaches or ransomware.

The Cost of Going Uninsured

While malpractice insurance is not legally required in most jurisdictions (except in states like Oregon and Idaho), practicing without it is a high-stakes gamble. The cost of a single claim can far exceed the annual premiums for coverage. For example, the average cost of defending a legal malpractice claim is estimated at $50,000-$100,000, with settlements or judgments often reaching six or seven figures in serious cases.

Without insurance, lawyers must bear these costs themselves, which can lead to financial ruin. Additionally, uninsured lawyers may struggle to attract clients, as many corporate and institutional clients require proof of malpractice coverage before engaging legal services. Going uninsured also increases stress and uncertainty, as every client interaction carries the potential for a career-ending lawsuit.

Factors Influencing Insurance Premiums

The cost of malpractice insurance varies based on several factors, including:

- Practice Area: High-risk specialties like personal injury, real estate, and intellectual property tend to have higher premiums due to the complexity and value of the cases involved.

- Firm Size: Larger firms with more attorneys and higher caseloads typically pay higher premiums, though economies of scale may reduce per-lawyer costs.

- Claims History: Lawyers with a history of claims or disciplinary actions may face higher premiums or difficulty obtaining coverage.

- Geographic Location: Premiums vary by state, reflecting differences in litigation rates, court systems, and local regulations.

- Coverage Limits: Policies with higher coverage limits or broader protections command higher premiums. Typical coverage limits range from $250,000 to $5 million per claim, with annual aggregate limits.

On average, solo practitioners can expect to pay $1,000-$3,000 annually for malpractice insurance, while larger firms may pay tens of thousands. Shopping around and comparing quotes from multiple insurers can help lawyers find cost-effective coverage.

Beyond Insurance: Proactive Risk Management

While insurance is a critical tool, it is not a substitute for sound risk management. Lawyers can further reduce their exposure to lawsuits by adopting best practices, such as:

- Clear Client Communication: Written engagement letters, regular updates, and transparent fee structures can prevent misunderstandings.

- Robust Documentation: Thorough record-keeping of client interactions, case progress, and legal research can provide a strong defense against claims.

- Continuing Education: Staying current on legal developments and ethical standards helps lawyers avoid errors.

- Conflict Checks: Rigorous screening for conflicts of interest before taking on new clients can prevent ethical violations.

- Cybersecurity Measures: Implementing strong data protection protocols reduces the risk of breaches that could lead to liability.

By combining insurance with proactive risk management, lawyers can create a comprehensive strategy to protect their practice.

The Broader Implications for the Legal Industry

The availability of malpractice insurance has far-reaching implications for the legal profession. It promotes access to justice by enabling lawyers to take on complex or high-risk cases without fear of personal financial ruin. It also fosters public trust in the legal system, as clients are more likely to engage attorneys who carry insurance, knowing they have recourse in the event of errors.

Moreover, insurance incentivizes ethical and competent practice. Insurers often provide risk management resources, such as training programs and practice guides, to help policyholders avoid claims. In turn, this contributes to higher standards of professionalism across the industry.

Conclusion

In an era of increasing litigation and professional scrutiny, malpractice insurance is an indispensable tool for lawyers. It shields practitioners from the financial and reputational damage of lawsuits, allowing them to focus on serving their clients with confidence. By covering defense costs, damages, and regulatory proceedings, insurance provides a critical safety net in a high-stakes profession. However, insurance is most effective when paired with proactive risk management strategies that minimize the likelihood of claims. As the legal landscape continues to evolve, malpractice insurance will remain a cornerstone of a resilient and trustworthy legal profession, ensuring that lawyers can navigate risks without compromising their commitment to justice.